Will they be the next cannabis giant to face de-listing notice from the NYSE ?

MF write

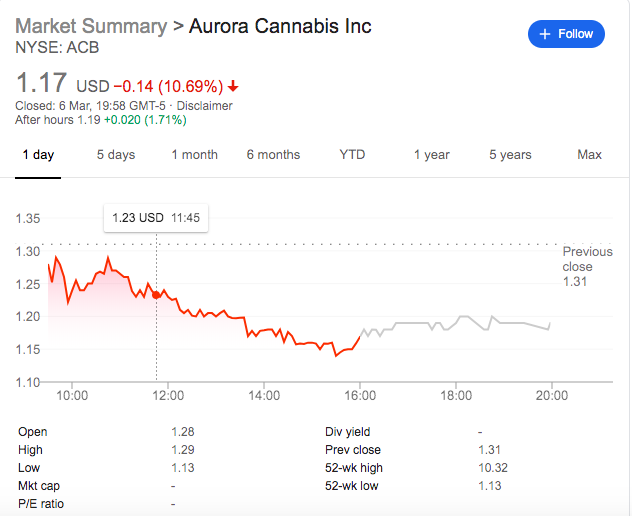

Aurora stock is now going for a mere $1.36 per share, and some investors may think it’s a bargain. After all, the company is still expected to be one of the leading producers of marijuana throughout Canada and has a presence in 24 countries outside of its home market.

But believing that a low share price is enough justification to buy into Aurora Cannabis could prove dangerous. Chances are that things are going to get worse for the company before they have a chance to get better.

On a more immediate level, investors should be worried about the company’s consistently shrinking share price. Being listed on the New York Stock Exchange (NYSE) has afforded Aurora improved volume-based liquidity, increased Wall Street coverage, and undoubtedly better investor visibility than if it were trading on the over-the-counter exchange. However, the NYSE has a share price minimum of $1 that’s required for continued listing. Aurora Cannabis isn’t there yet, but amid the strongest point rally in the history of the Dow Jones Industrial Average, on Monday, March 2, Aurora’s stock hit a new 52-week low of $1.31.

If Aurora’s shares were to dip below $1 and stay there for a period of 30 days, the company almost certainly would draw a delisting notice from the NYSE. The company would have remediation pathways available, such as delaying delisting and hoping its stock regains a $1 minimum share price. Then again, “hope” isn’t a valid long-term strategy.

There’s also the possibility of a reverse stock split, which would reduce the number of shares outstanding (currently 1.17 billion) and pump up the company’s share price. Unfortunately, reverse stock splits are typically viewed as a sign of weakness and may lead to further downside.

The intermediate forecast and long-term outlook aren’t looking too hot, either

Even if Aurora Cannabis somehow manages to skirt a delisting notice from the NYSE, its balance sheet remains an utter mess that’s not conducive to growth or market share expansion.

On one hand, Aurora Cannabis ended its fiscal second quarter (ended Dec. 31, 2019) with $156.3 million Canadian in cash and CA$26.1 million in marketable securities. This might sound like a healthy capital balance but it’s nowhere near sufficient given the company’s own expectations of CA$373.6 million in liabilities over the next 12 months and close to CA$1.3 billion in liabilities over the next four to five years.

With pretty much all avenues to traditional funding closed off and no equity deal signed, Aurora’s only means of raising capital continues to be to sell its own stock. After ballooning its outstanding share count by 1.15 billion since June 30, 2014, it’s no wonder shareholders have taken it on the chin.

Read the full article

https://www.fool.com/investing/2020/03/06/things-are-about-to-get-worse-for-aurora-cannabis.aspx